The deployment segment of the AI in fintech market is bifurcated into cloud and on-premises. Under this segment, the cloud category accounted for the larger market share in 2020, because the cloud environment enables AI to learn from historical data, make suggestions, and detect current norms. AI and cloud can together deliver improved digital security, increased productivity, and excellent efficiency in terms of information handling and accuracy.

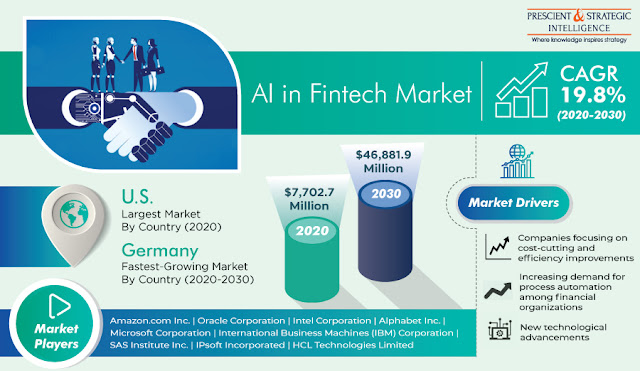

Owing to these advantages, AI-enabled cloud solutions help avoid human errors during data analysis. In the recent past, North America was the largest user of AI-enabled fintech solutions, due to the presence of developed IT infrastructure and high fintech adoption rate in the region. Additionally, the mounting investments being made in the fintech sector and increasing penetration of 5G technology will also fuel the integration of AI solutions in the fintech sector.

Besides, the mounting focus of the U.S. federal government on encouraging the incorporation of AI technology in the financial and security industries will also contribute to the digital transformation of these sectors. Whereas, the APAC AI in fintech market is expected to display the fastest growth during the forecast years (2021–2030).

This will be on account of the increasing number of government initiatives regarding the adoption of AI and IoT technologies across industries, flourishing economy, and surging demand for latest technologies in the region. Moreover, the heavy investments being made in the development of IT infrastructure will also facilitate the market growth in the region.

Therefore, the soaring focus of financial institutions on process automation and the rising availability of innovative payment platforms will encourage the adoption of AI-enabled fintech solutions globally.

Owing to these advantages, AI-enabled cloud solutions help avoid human errors during data analysis. In the recent past, North America was the largest user of AI-enabled fintech solutions, due to the presence of developed IT infrastructure and high fintech adoption rate in the region. Additionally, the mounting investments being made in the fintech sector and increasing penetration of 5G technology will also fuel the integration of AI solutions in the fintech sector.

Besides, the mounting focus of the U.S. federal government on encouraging the incorporation of AI technology in the financial and security industries will also contribute to the digital transformation of these sectors. Whereas, the APAC AI in fintech market is expected to display the fastest growth during the forecast years (2021–2030).

This will be on account of the increasing number of government initiatives regarding the adoption of AI and IoT technologies across industries, flourishing economy, and surging demand for latest technologies in the region. Moreover, the heavy investments being made in the development of IT infrastructure will also facilitate the market growth in the region.

Therefore, the soaring focus of financial institutions on process automation and the rising availability of innovative payment platforms will encourage the adoption of AI-enabled fintech solutions globally.

Comments

Post a Comment